The Quiet Money

Why the best capital is quiet — and why sending more decks is not the answer.

A founder I know spent eighteen months on his Series A. Strong company, real revenue, decent traction. He sent his deck to two hundred and forty investors. He took meetings with sixty-eight of them. He closed in the end, but the round took twice as long as it should have, and the lead came from someone he met by accident at a conference, not from anyone in his outreach list.

I asked him afterwards what he’d do differently. He said the obvious thing. I’d start the outreach earlier.

I think he had it backwards.

The problem wasn’t that he sent his deck to too few investors. The problem was that he sent his deck to two hundred and forty people without first knowing which of them actually fit, and the rest of his fundraise was spent paying the cost of that initial mismatch.

This is the most common founder mistake I see, and it has gotten worse, not better, as the tools for outreach have multiplied. The conventional wisdom is that raising capital is a numbers game — more decks, more meetings, more activity, more chance of a yes. The conventional wisdom is wrong. The capital that matters does not respond to volume. It responds to fit, to trust, to evidence, and to timing. None of those four things are improved by sending more decks.

This is the first of two pieces on what to do instead.

There are two capital markets in the world. One is loud. The other is quiet. Almost everyone writing about fundraising describes only the loud one.

The loud market is the one you’ve read about. The named institutions that publish their thinking, hire press teams, attend conferences, give interviews, and post on LinkedIn. Yale’s endowment under David Swensen, returning 13.7% annualised over thirty years and writing about it openly. CalPERS with $500 billion under management and a public allocation framework. The named family offices that have hired comms staff. The funds whose partners give podcast interviews. This is the market every emerging fund manager chases, and it is the market every founder tries to crack with cold outreach.

The quiet market is the one that quietly does the work. The single family offices that don’t have websites. The multi-generational private wealth structures whose principals never appear at SuperReturn. The advisory networks that introduce capital between people who already know each other and have known each other for decades. The investment offices of families whose names you would recognise but whose allocation decisions you have never read about.

Some context for how big the quiet market actually is, because the numbers are easy to underestimate.

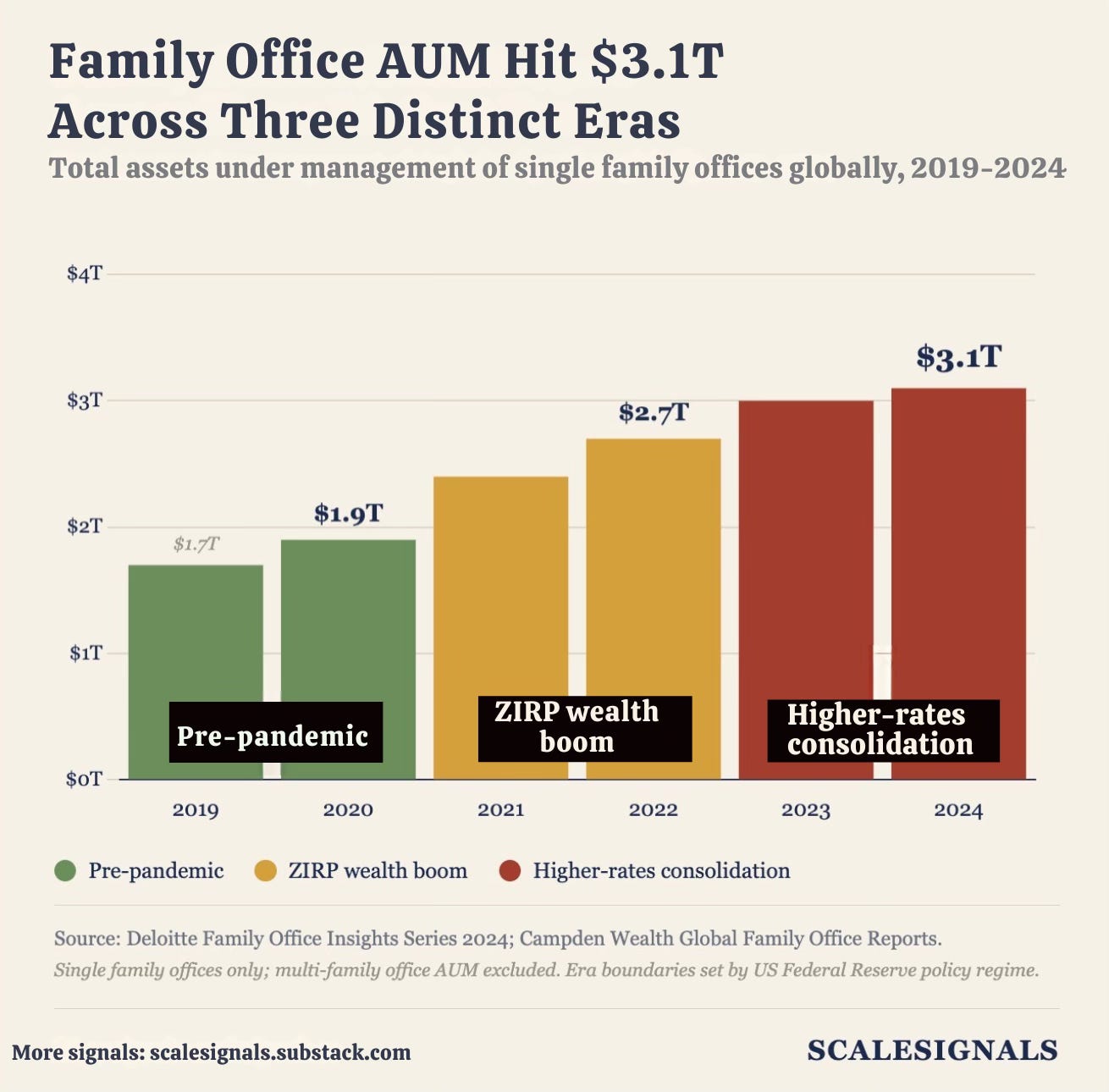

CHART 1 — Family Office AUM Hit $3.1T Across Three Distinct Eras

Notice what the chart shows and what it doesn’t. The boom years are what you’d expect — a liquidity wave lifted everyone, family offices included. The consolidation years are what you wouldn’t. The rate cycle was supposed to compress private wealth in alternatives. It didn’t compress this layer. The quiet market kept allocating, kept compounding, and finished the cycle larger than it started. That is not a cyclical phenomenon. That is a structural reallocation of capital, and it has happened mostly outside the public fund-of-funds layer where this kind of growth would normally show up.

According to Deloitte’s most recent Family Office Insights work, the number of single family offices globally has grown from roughly 6,000 in 2019 to over 8,000 by 2024. Total AUM crossed $3.1 trillion. Campden Wealth’s research shows these structures consistently allocate around 24% of their portfolios to private equity and venture capital combined — a higher allocation than most public pension funds carry, and higher than most endowments outside the top quartile.

This is not a small market. It is structurally larger than the entire US public pension fund alternative allocation. It is allocated by people whose names appear in the press only when they buy a sports team. And it is the part of the capital ecosystem that the loud playbook cannot reach.

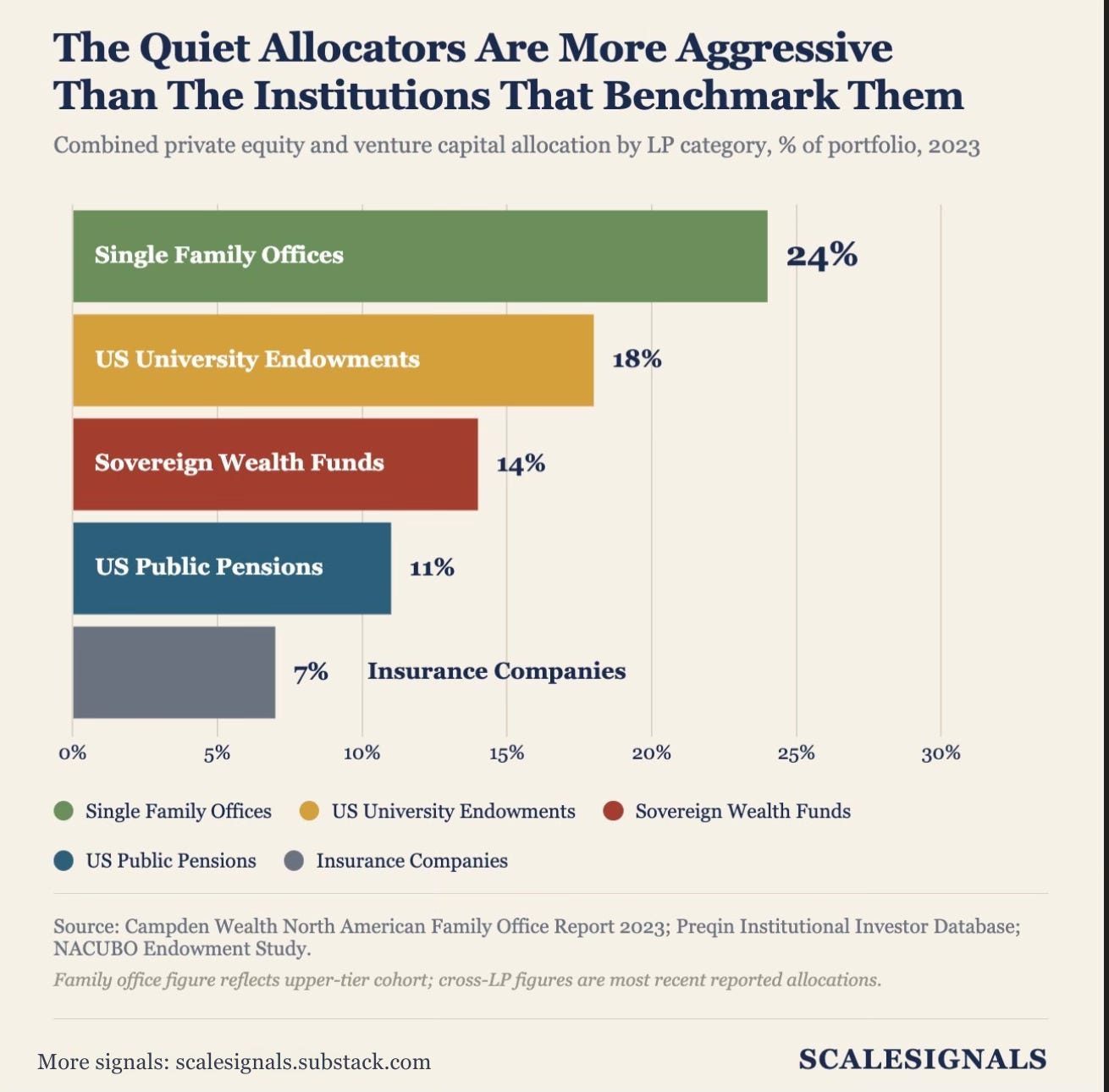

CHART 2 — The Quiet Allocators Are More Aggressive Than the Institutions That Benchmark Them

The numbers in this chart are the structural answer to a question almost nobody asks. Why are the institutions that publish the most also the ones least aggressively allocated to alternatives? The answer is that publishing has a cost. An institution that writes annual reports and gives interviews has to defend its allocation publicly, and public defensibility tends to compress risk-taking. The institutions that don’t publish don’t have that constraint. They allocate more aggressively to private markets because they don’t have to explain themselves to anyone who didn’t grow up at the same dinner table.

Here is the part that matters most for anyone reading this who is on the founder side of the relationship, or who is running an emerging fund.

The quiet market does not respond to outreach the way the loud market does. It does not respond to better decks, more meetings, sharper subject lines, or volume. It responds to four specific things, and almost no founder or emerging manager I have ever met has thought about them in this order.

Fit. Quiet capital backs themes and patterns it has been thinking about for years, sometimes decades. The principals running these structures are not making allocation decisions on the basis of a one-hour pitch. They are matching what shows up to them against a thesis that has been forming through every conversation, every previous investment, every cycle they have lived through. A founder who sends a generic outreach is asking quiet capital to do the work of figuring out whether the company fits the thesis. Quiet capital will not do that work. It will pass.

The implication for founders is that the highest-leverage hour you can spend in a fundraise is not writing a better deck. It is researching, in real depth, the specific allocation history and active thesis of the small number of capital sources that actually fit your stage, sector, and geography. Most founders do this for ten or twenty investors and then default to volume for the rest. That is exactly backwards. The quality of your fit work is the single biggest determinant of how long your fundraise takes.

Trust. Quiet capital allocates almost entirely through trusted introductions. Not because cold outreach is forbidden, but because trust does the diligence work that nobody has time to do otherwise. A warm introduction from a trusted source signals, before any deck has been read, that someone the principal already trusts has staked a small piece of their own credibility on the meeting being worth taking. This is enormous. It is also unpurchasable. You cannot buy your way to a warm introduction. You can only earn it, usually over years, through your own pattern of behaviour with the people who have the standing to make those introductions.

The implication is that the most valuable people to know in your sector are not the investors. They are the operators, advisors, and second-tier capital sources who sit one layer away from the quiet market and have the standing to introduce. These relationships are built before you are raising, not during. The founder who starts building them when they need capital is already too late.

Evidence. Quiet capital looks for evidence, not narrative. The pitch deck is a narrative document. The data room is an evidence document. Most founders spend ninety percent of their fundraise effort on the deck and ten percent on the data room. The principals of the quiet market read the deck once and spend the next three weeks in the data room. What they want to see is not your story but your operating discipline. Cohort tables that hold up under questioning. Unit economics with real assumptions named. Customer interviews you didn’t curate. Hire-fire decisions documented honestly. The kind of evidence that requires no embellishment because it is already enough.

The implication is that the work of preparing for a fundraise is not the work of building a deck. It is the work of building a company whose evidence layer is complete, accurate, and honest. Founders who try to assemble this in the four weeks before a raise are visible from a long way off. Founders who have been building it as part of the operating cadence are visible from the same distance — but for the opposite reason.

Timing. Quiet capital operates on its own clock, not yours. A family office that has been allocating to one thesis for ten years will not accelerate its decision because your runway is short. The principals are not reacting to your urgency. They are matching what comes across their desk against where they are in their own allocation cycle. A founder who shows up at the wrong moment in that cycle is unlikely to be backed even if the fit, trust, and evidence are all in place.

The implication is that fundraising timing is partly outside your control, and the founders who succeed treat fundraising as a continuous activity rather than an event. The relationships are built across cycles, not within one. The conversation that closes a Series B in 2027 may have started as a coffee in 2025 with no specific raise in mind. This is not how most founders are taught to think about fundraising. It is how the founders who close cleanly actually behave.

Notice what is and isn’t on this list. Volume is not on it. Outreach intensity is not on it. Sending more decks is not on it. None of the four things the quiet market actually responds to are improved by activity alone. They are improved by preparation, by relationships built over time, by operating discipline, and by patience.

This is why the conventional fundraising playbook fails so often against the part of the capital market that matters most. The playbook tells founders to optimise for volume. The market it actually has to win in is allergic to volume. The mismatch is structural, and it is why even strong companies often spend twice as long raising as they should.

For emerging fund managers the same logic applies, with one additional layer. An emerging GP whose entire LP base consists of names you can find on Google has access only to the loud market — the over-fished pond. Their information edge is small. Their fundraising cycle is long. Their pressure to deploy is high. An emerging GP who can name three LPs you have never heard of and never could have heard of has access to the quiet market. This changes their patience, their concentration risk tolerance, and their willingness to back unconventional founders. It is one of the most under-priced asymmetries in venture and private equity, and almost nobody talks about it because the people who know it are the people whose advantage depends on it not being talked about.

The future of capital raising — for founders and for emerging managers — is not more access. It is better preparation before access.

This is the strategic shift that the next decade of fundraising will be defined by. The tools for outreach have made volume effectively free. Every founder can now send a thousand emails for the same effort it used to take to send fifty. The result is that volume has stopped being a competitive advantage. The bar has shifted. The advantage now sits with the people who arrive at the conversation already prepared — who know who they’re talking to, what that person’s thesis is, what evidence will move them, and whether the timing of the relationship matches the timing of the raise.

This is harder work than sending more decks. It requires the kind of preparation most founders skip because it doesn’t feel like progress. It requires building relationships in advance of need. It requires operating discipline that produces evidence as a by-product of running the company well. And it requires a different kind of patience — the willingness to invest in conversations that may not pay off for two years, with people who may never write a cheque, because the network those conversations build is what eventually leads to the room where the cheque actually gets written.

For founders raising right now, the highest-leverage thing you can do this week is not send more decks. It is to take your current target list and cut it by 80%. Keep only the investors who genuinely fit your stage, sector, and thesis. Then spend the time you would have spent on the cut investors doing real fit work on the ones that remain — reading their portfolio, identifying their active themes, finding warm introductions, preparing for the specific conversation each one will want to have. You will close faster with twenty well-prepared conversations than with two hundred unprepared ones. Every founder who has raised cleanly will tell you the same thing.

For emerging managers, the highest-leverage thing you can do is the same exercise applied to your LP base. The institutional LPs you can find on the internet are the wrong starting point unless you have a compelling differentiated angle that lets you cut through the over-fished part of the market. The right starting point is the quiet layer — the family offices, the private wealth structures, the advisory networks. Building access to that layer takes years. The managers who eventually run sustainable fund franchises started building it before they raised their first fund.

Next Sundays’s Briefing is part two — How to Be Ready Before You Raise. It walks through the specific preparation framework that converts the four things the quiet market responds to into actual founder and GP behaviour. The principles in this piece are the why. Next week’s piece is the how.

—

Ben Botes is an active GP, 4x exited founder, and MD of Caban Group. He has spent 24 years across venture, private equity, governance, and scale-ups, and is the author of the Amazon bestseller Unstoppable Growth*. Through ScaleSignals, he helps founders and fund managers stop wasting their raise on the wrong investors by building stronger evidence, clearer investor fit, and better capital conversations.*

Next Tuesday — Part 2 of the Decision Architecture series: how to diagnose which layer of your decision architecture is failing right now.

Next Sunday — How to Be Ready Before You Raise. The preparation framework that converts the four signals quiet capital responds to into actual founder behaviour.

ScaleSignals paid tiers launch end of June. Membership £99/year for founders and emerging managers building the practical preparation layer this Briefing describes. Pro £400/year for deeper investor tools, prep packs, and workflow access. Institutional from £5,000/year for GPs, LPs, and teams needing the full intelligence layer.

Strong thesis and very clear distinction between volume vs alignment. The “loud vs quiet market” framing is especially effective and memorable. The only gap is that it leans slightly abstract in places where a bit more concrete examples would make it even sharper.

Great article man, actually interesting

Subscribed, would love to have you along too🙂🙌