The Deal Read: Four rounds from May, decoded from both sides of the table — and why the same structure can mean opposite things

Capital Signals Briefing — June 2026

Most people read a funding announcement the way they read a scoreboard. A number, a name, a stage. Company raises $700 million; the market is hot. Company raises $45 million; the market is smaller. The figure becomes the story, and the story becomes a lesson the reader files away for their own raise: this is what good looks like, this is the bar, this is the route.

The figure is almost never the story. What a round actually tells you is buried one level down, in how it was built — which instruments, which investors, which risk sat with whom. Two companies can announce the same headline number and have done two completely different things with it. A founder who copies the number without reading the structure copies the wrong thing, and pays for it with a quarter they will not get back.

May produced an unusually clean set of teaching cases. Four rounds, four structures, and between them almost the entire grammar of how private capital is priced right now — from a strategic land-grab in Silicon Valley to a Shariah-compliant debt facility in West Africa. I have sat on both sides of these conversations: the GP deciding what a structure signals, and the founder trying to read what an investor actually means. From that seat, here is what these four rounds are really saying.

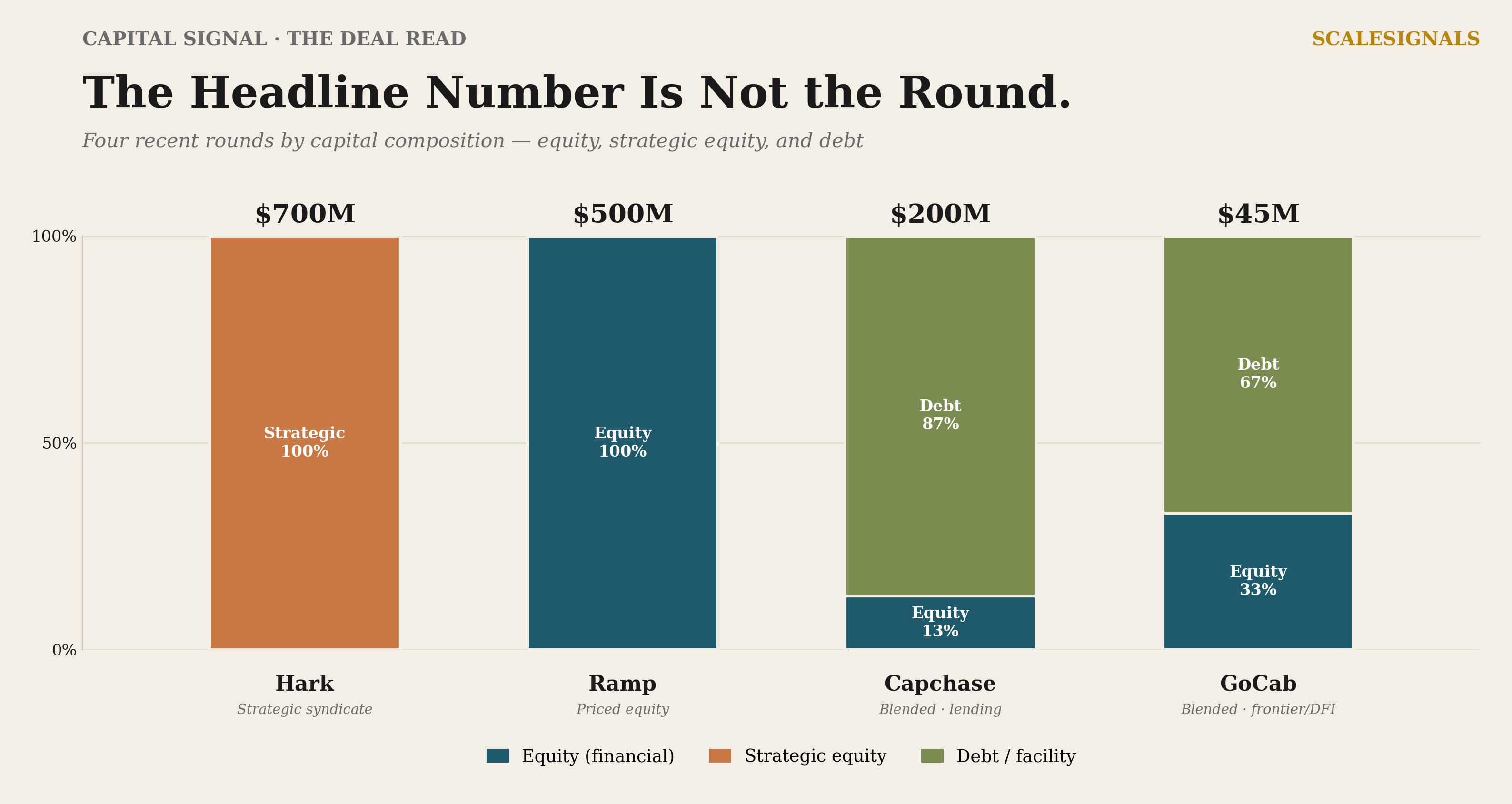

When the cap table is the product

Start with the round everyone has already read about. Hark, a roughly twelve-month-old AI lab, raised over $700 million in a Series A at a $6 billion post-money valuation, led by Parkway Venture Capital. The participant list is the part worth your attention: Nvidia, AMD Ventures, Intel Capital, Qualcomm Ventures, ARK Invest, Brookfield, Greycroft, Salesforce Ventures and more.

Read that list again, slowly, because it contains a thing that does not normally happen. Nvidia, AMD, Intel and Qualcomm are direct competitors. They do not share cap tables as a rule, because backing the same horse undercuts the whole point of a proprietary bet. Four of them on one Series A is not four investors who independently liked the company. It is the chip industry collectively buying an option on what might become the next hardware interface — and none of them wanting to be the one who sat it out. The structure is a hedge dressed as a financing.

This is what I mean by reading a round from the inside. A founder looking at Hark sees the lesson “raise enormous money pre-product if your vision is big enough.” That lesson is false, and acting on it is expensive. The truth is that this round was not priced on Hark’s fundamentals — there is barely a product to price. It was priced on a serial founder who had already built two companies worth more than a billion dollars each, who put in $100 million of his own capital first, and on a strategic land-grab among chipmakers who can each afford to be wrong. Strip any one of those three conditions away and the round does not exist.

Strategic capital prices differently from financial capital. A financial investor asks what the company is worth. A strategic investor asks what it is worth to them to have a seat — to secure supply, to deny a rival, to learn. Those are not the same question, and the cheque that follows from the second one tells you almost nothing transferable about your own raise unless you can offer a strategic reason of your own. The most common way founders waste a quarter is chasing strategic money with a financial pitch, never understanding that the investor was solving a different equation the whole time.

The full Deal Read — the three remaining structures, and the framework for reading which one applies to your own raise — continues below for paid subscribers.